Course

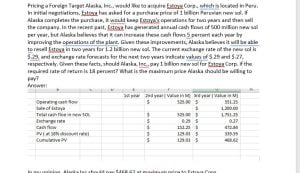

- Question: Pricing a Foreign Target Alaska, Inc., would like to acquire Estoya Corp., which is located in Peru. In initial negotiations, Estoya has asked for a purchase price of 1 billion Peruvian new sol. If Alaska completes the purchase, it would keep Estoya’s operations for two years and then sell the company. In the recent past, Estoya has generated annual cash flows of 500 million new sol per year, but Alaska believes that it can increase these cash flows 5 percent each year by improving the operations of the plant. Given these improvements, Alaska believes it will be able to resell Estoya in two years for 1.2 billion new sol. The current exchange rate of the new sol is $.29, and exchange rate forecasts for the next two years indicate values of $.29 and $.27, respectively. Given these facts, should Alaska, Inc., pay 1 billion new sol for Estoya Corp. if the required rate of return is 18 percent? What is the maximum price Alaska should be willing to pay?

- Question: Feasibility of a Divestiture Merton, Inc., has a subsidiary in Bulgaria that it fully finances with its own equity. Last week, a firm offered to buy the subsidiary from Merton for $60 million in cash, and the offer is still available this week as well. The annualized long-term risk-free rate in the United States increased from 7 to 8 percent this week. The expected monthly cash flows to be generated by the subsidiary have not changed since last week. The risk premium that Merton applies to its projects in Bulgaria was reduced from 11.3 to 10.9 percent this week. The annualized long-term risk-free rate in Bulgaria declined from 23 to 21 percent this week. Would the NPV to Merton, Inc., from divesting this unit be more or less than the NPV determined last week? Why? (No analysis is necessary, but make sure that your explanation is very clear.)

- Question: Financing Decision Drexel Co. is a U.S.-based company that is establishing a project in a politically unstable country. It is considering two possible sources of financing. Either the parent could provide most of the financing, or the subsidiary could be supported by local loans from banks in that country. Which financing alternative is more appropriate to protect the subsidiary?

- Question: Financing Trade-Offs Pullman, Inc., a U.S. firm, has been highly profitable but prefers not to pay out higher dividends because its shareholders want the funds to be reinvested. It plans for large growth in several less developed countries. Pullman would like to finance the growth with local debt in the host countries of concern to reduce its exposure to country risk. Explain the dilemma faced by Pullman, and offer possible solutions.

- Question: Financing Decision In recent years, several U.S. firms have penetrated Mexico’s market. One of the biggest challenges is the cost of capital to finance businesses in Mexico. Mexican interest rates tend to be much higher than U.S. interest rates. In some periods, the Mexican government does not attempt to lower the interest rates because higher rates may attract foreign investment in Mexican securities.

- How might U.S.-based MNCs expand in Mexico without incurring the high Mexican interest expenses when financing their expansion? Are any disadvantages associated with this strategy?

- Are there any additional alternatives for the Mexican subsidiary to finance its business itself after it has been well established? How might this strategyaffect the subsidiary’s capital structure?

6. Question: Exchange Rate Effects

- Explain the difference in the cost of financing with foreign currencies during a strong-dollar period versus a weak-dollar period for a U.S.firm.

- Explain how a U.S.-based MNC issuing bonds denominated in euros may be able to offset a portion of its exchange rate risk.

7. Question: Borrowing Combined with Forward Hedging Cedar Falls Co. has a subsidiary in Brazil, where local interest rates are high. It considers borrowing dollars and hedging the exchange rate risk by selling the Brazilian real forward in exchange for dollars for the periods in which it would need to make loan payments in dollars. Assume that forward contracts on the real are available. What is the limitation of this strategy?

8. Question: Financing Decision Cuanto Corp. is a U.S. drug company that has attempted to capitalize on new opportunities to expand in Eastern Europe. The production costs in most Eastern European countries are very low, often less than one-fourth of the cost in Germany or Switzerland. Furthermore, there is a strong demand for drugs in Eastern Europe. Cuanto penetrated Eastern Europe by purchasing a 60 percent stake in Galena, a Czech firm that produces drugs. 1. Should Cuanto finance its investment in the Czech firm by borrowing dollars from a U.S. bank that would then be converted into koruna (the Czech currency) or by borrowing koruna from a local Czech bank? What information do you need to know to answer this question? 2. How can borrowing koruna locally from a Czech bank reduce the exposure of Cuanto to exchange rate risk? 3. How can borrowing koruna locally from a Czech bank reduce the exposure of Cuanto to political risk caused by government regulations?

ANSWER

………….please click the icon below to purchase the answer at $10